My disgust with the lies and disinformation campaigns of the right wing and the GOP in regard to the nature and implementation of the Affordable Care Act, known colloquially as “Obamacare”, has pretty much maxed out. I don’t think I have seen such a non-stop smoke screen of blatant dishonesty by political figures since the McCarthy era.

Bottom line, this is a law that was created/invented/dreamed up by the right wing Heritage Foundation, as a way to keep health insurance in the hands of private corporations. It was implemented as exactly that in Mass, by Romney, when governor, with the required mandate, and subsidies for the poor to help them buy insurance.

Here is the original document, in .pdf format, as authored by Stuart M. Butler as part of Heritage Foundation lecture series of publications, published in 1989, The Heritage Lectures 218 Assuring Affordable Health Care for All Americans. This is the document that included the original idea of the required mandate, in order to insure participation that would allow the use of the private insurance industry to scale and cover the idea.

Not until it was the only law Obama and the Democrats could get through Congress did the GOP discover that the law they had supported wholeheartedly was suddenly socialism and an existential threat to America. Because $DEITY knows, owning health insurance is right up there next to Communism and Godlessness.

I recently responded to a throwaway critical remark about the ACA to a business colleague that I know indirectly, because he deals with an organization for whom I wrote a sales fulfillment and history database which I still maintain on a consulting basis.

I realized later that I had been, well, pretty blunt in my response to his remark, which was spoken as a typical throwaway cut at Obamacare, and obviously expecting me to agree with the joke. Which I did not.

So I emailed him to let him know I hoped he had not been personally offended, and tried to explain the context, and that it was not aimed at him personally, but just reflected my impatience with the disinformation echo chamber, which, quite frankly, I consider to be perhaps the greatest existential threat to our nation currently.

You cannot run a nation on lies. Other than into the ground.

The fact is, I have in fact reached the point where my patience with the echo chamber of disinformation in our media and coming out of the mouths of our politicians is just exhausted. And that applies to both parties. You cannot run a nation, except into the ground, unless the debate is truth and fact based, and we have come unhinged on that regard. As far as I am concerned, 98% of the GOP and about 80% of the Democratic incumbents in Congress should be removed from office, and replaced with people who actually care about truth, justice, and the American Way. And by that, I do not mean people who enforce their religious and bigoted beliefs on others, I mean just the absolute opposite.

By that I mean politicians who invest in jobs, and restoring our crumbling infrastructure, and building a society where every one has access to health care and a good job, and that wealth is not concentrated in the hands of 1% of the population, and 400 families. Which is where we are at the moment.

Today the top 1 percent of Americans control 43 percent of the financial wealth (see the pie chart below) while the bottom 80 percent control only 7 percent of the wealth. Incredibly, the wealthiest 400 Americans have the same combined wealth as the poorest half of Americans — over 150 million people.

Fact is, as far as I am concerned, the only viable solution to health care insurance is single payer, Medicare for all. Did you know that the overhead costs for Medicare is only 5%? And that the ACA for the first time forces private insurance to spend at least 80% on payments to the insured, with only a maximum of 20% profit / overhead allowed? Some companies used to charge as high as 50% overhead, although most were probably around the 30 – 35% suck up the money range.

If you would take a couple of minutes, look at these links for a straightforward factual explanation of the nature and impact of the Affordable Health Care Act (Obamacare) on what percentages of the populace, and with what results.

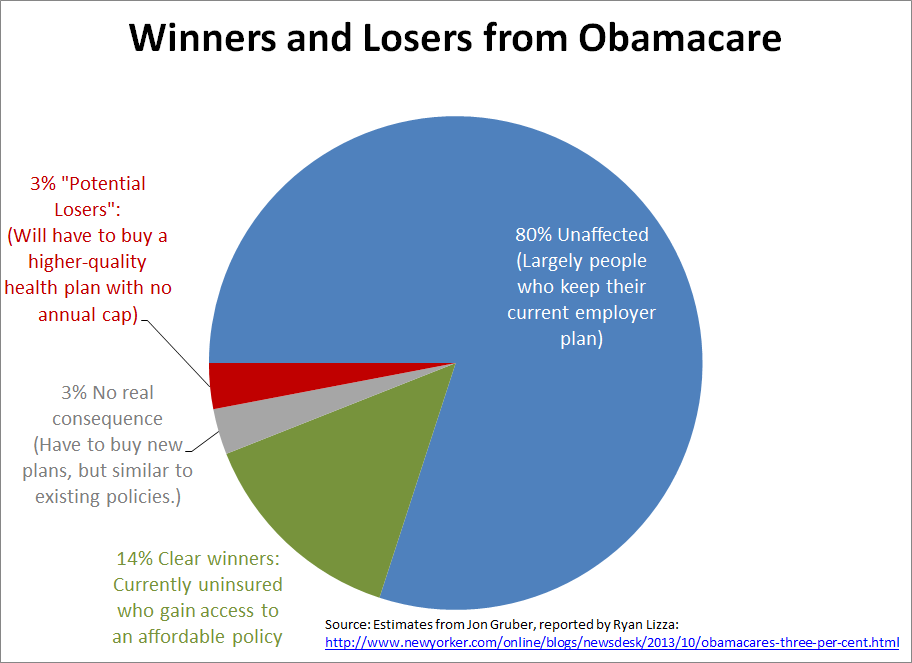

First, from “New Republic” magazine, the Winners and Losers from Obamacare pie chart, which is where I got the 3% figure. The article and the chart explain it clearly.

Right mouse and view image for higher resolution and source attribution.

And in a country of 300 million, 3 percent still represents a lot of people. But to stick with one of my themes, all policy choices involve trade-offs. The higher premiums that some people will now pay for insurance are the price of a system that makes coverage available to all, at uniform prices, regardless of medical condition—and that establishes a basic set of benefits that no plan may omit. Obamacare attempts to minimize the impact by providing subsidies, generous enough so that people stuck with higher bills can, by and large, afford them. But there’s no denying that some people will pay more, whether because rates go up or they have to buy more expensive plans.

Is the tradeoff worth it? That’s obviously a matter of opinion. And a true accounting would include all of the law’s costs (like higher taxes on the wealthy, lower Medicare spending on various medical providers, etc.) as well as all the benefits (new incentives for quality care, more prescription drug coverage for seniors, etc.). But the old system had its costs, too—costs that even people paying low premiums sometimes faced.

After all, if you were holding one of those cheap policies, you might get sick and face crippling medical bills. Or you might end up with a condition that, later on, subjected you to higher premiums and left you unable to switch policies. As Gruber told Lizza, “no law in the history of America makes everyone better off.”

This article from HuffingtonPost discusses the controversial examples:

There’s been a lot of talk lately about people getting letters from their health insurance carriers canceling their policies because of Obamacare. What’s really going on here?

Wait, Obama killed my health insurance? Oh %$@*, I’m uninsured now!

Not quite. First off, this affects a pretty small sliver of the U.S. population: the people who buy health insurance directly, rather than the 80 percent who get it from their jobs or a government program like Medicare or Medicaid, or the 15 percent who have no health insurance at all.

Estimates vary, but the Census Bureau says this figure is about 4 percent of Americans, which comes to about 11 million people. A lot of those folks are finding out that the health insurance plans they have this year aren’t going to be sold anymore. How many? Hard to say, with reports ranging from a few hundred thousand to millions. (And their coverage isn’t changing today; it’s changing next year.)

I’m one of those people! Why would Obama make health insurance companies cancel my plan? Seems mean.

The fact is, some health insurance on the market today is just lousy. That’s a big reason why even people who have insurance can go bankrupt when their medical bills start piling up.

Health insurance you bought for yourself before might have been (or seemed) perfectly okay, but there’s a good chance it had big holes in it — the kind people tend to only find out about when they incur expensive doctor and hospital bills. And if you have a pre-existing condition, or you’re older, or you’re a woman, you have been paying more for that insurance.

But not all the insurance plans being canceled are lousy. Some people really do like their plans, and they’re losing them because of relatively small differences in new Affordable Care Act rules.

The law standardizes health insurance plans by mandating that they cover a basic set of benefits, including hospitalizations, prescription drugs and maternity care, that many insurance products on today’s market don’t. Obamacare also limits total annual out-of-pocket expenses to $6,350 for a single person, in order to protect people against going broke when they get sick.

…

The news has been filled with repeated debunkings of the reported awful experiences of people discovering their insurance policies cannot be kept as is.

And in almost every case, it turns out their policies were over priced and did not provide for real coverage, and that replacement policies that cost less and covered more were available on the insurance exchanges.

My favorite example was the woman reported unhappy, who had not bothered to check to see what was available. Her policy costing over $600 a month would have covered almost nothing is she had experienced e.g. a cancer. The rebuttal showed how a cost of $120,000 to treat would have left her with a bill for about $116,000 of the cost. For less than $300, she can now get a policy that has a maximum out of pocket outlay of $6,300 per year. Every year.

Sean Hannity did a story on the horrors faced by several families. And then some journalist managed to fact check the stories. And the results were, well laughable is charitable.

Sean Hannity has been fact-checked, and the results aren’t pretty.

In an article posted on Salon on Friday, Eric Stern “re-reported” a recent episode of Fox News’ “Hannity” during which host Sean Hannity invited six guests to tell their Obamacare “horror stories.”

According to Stern, there was a lot more to each of the guests’ stories than Hannity let on. Stern decided to conduct his own investigation by separately interviewing each guest, and what he said he found was not that the guests were cheated by Obamacare, but rather that they had tried very little, if at all, to participate in the ACA.

Stern accused the Fox News host of using “fake evidence” to “exploit people’s ignorance and falsely point to imaginary boogeymen,” deeming it all a part of the “Fox News lie machine.”

…

“I don’t doubt that these six individuals believe that Obamacare is a disaster; but none of them had even visited the insurance exchange,” Stern wrote. “Hannity is not entitled to point to Paul’s behavior as an “Obamacare train wreck story” and maintain any credibility that he might have as a journalist.”

The bill includes the mandate in order to insure as many as possible in order to cover the costs. That is how insurance works. That is why the Heritage Foundation designed the idea that way to begin with.

Finally, here is a nice summary from MediaMatters web site, 15 Myths The Media Should Ignore During Obamacare Implementation, with every lie and talking point debunked completely:

Myth #1: Congress Is “Exempt” From The Affordable Care Act

Myth #2: Premium Prices Will Increase Due To Health Care Law

Myth #3: The Affordable Care Act Includes Death Panels

Myth #4: Shutting Down Government Over Obamacare Funding Will Stop Health Care Law

Myth #5: The Affordable Care Act Is “Socialized Medicine” And A “Government Takeover” Of Health Care

Myth #6: People Will Be Able To Commit Subsidy Fraud On The Exchanges

Myth #7: Obamacare “Narrow Networks” Will Constrain Health Choices

Myth #8: The Affordable Care Act Is Bad For Women

Myth #9: The Affordable Care Act Covers Abortions

Myth #10: The Affordable Care Act Is A Job Killer

Myth #11: With Full Access To Medical Records, The IRS Will Discriminate Against Conservatives

Myth #12: Navigators Will Abuse Private Information

Myth #13: Obamacare Mandates Doctors To Ask Patients About Sexual History

Myth #14: The ACA’s Medicaid Expansion Will Force Doctors To Turn Away Patients

Myth #15: The ACA Is To Blame For A Projected 30 Million People Who Will Remain Uninsured

15 Myths The Media Should Ignore During Obamacare Implementation

And just to look at one more example of a person whose complaint was amplified through the disinformation echo chamber, but where a main stream journalism organization, in this case the LA Times, die some actual journalism, researched the facts, and pointed out how far from the truth the initial claims were.

The bottom line is that Cavallaro’s assertion that “there’s nothing affordable about the Affordable Care Act,” as she put it Tuesday on NBC Channel 4, is the product of her own misunderstandings, abetted by a passel of uninformed and incurious news reporters.

I talked with Cavallaro, 60, after her CNBC appearance. Let’s walk through what she told me.

Her current plan, from Anthem Blue Cross, is a catastrophic coverage plan for which she pays $293 a month as an individual policyholder. It requires her to pay a deductible of $5,000 a year and limits her out-of-pocket costs to $8,500 a year. Her plan also limits her to two doctor visits a year, for which she shoulders a copay of $40 each. After that, she pays the whole cost of subsequent visits.

This fits the very definition of a nonconforming plan under Obamacare. The deductible and out-of-pocket maximums are too high, the provisions for doctor visits too skimpy.

As for a replacement plan, she says she was quoted $478 a month by her insurance broker, but that’s a lot more than she’ll really be paying. Cavallaro told me she hasn’t checked the website of Covered California, the state’s health plan exchange, herself. I did so while we talked.

Here’s what I found. I won’t divulge her current income, which is personal, but this year it qualifies her for a hefty federal premium subsidy.

At her age, she’s eligible for a good “silver” plan for $333 a month after the subsidy — $40 a month more than she’s paying now. But the plan is much better than her current plan — the deductible is $2,000, not $5,000. The maximum out-of-pocket expense is $6,350, not $8,500. Her co-pays would be $45 for a primary care visit and $65 for a specialty visit — but all visits would be covered, not just two.

Is that better than her current plan? Yes, by a mile.

…